La velocidad de liquidación como palanca de flujo de caja: cripto T+0 frente a redes de tarjetas T+2

Todo el mundo evalúa a los proveedores de pago basándose en las comisiones. Casi nadie los evalúa según cuándo llega realmente el dinero, y esa cifra determina silenciosamente cuánto de tus propios ingresos puedes utilizar y cuándo.

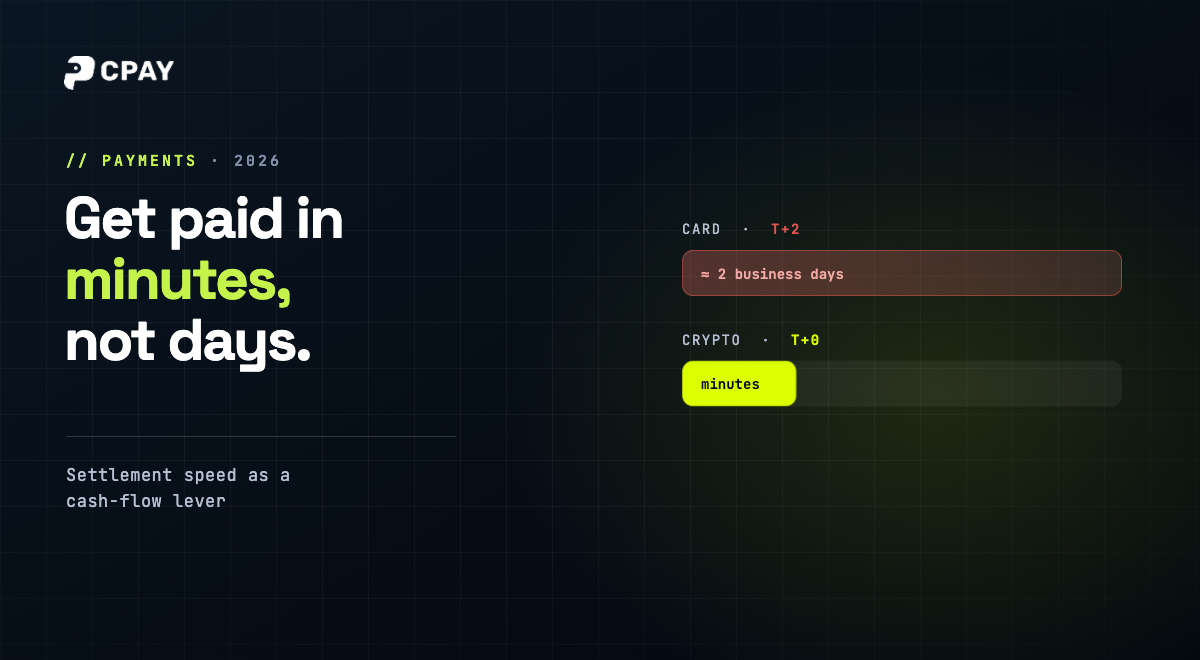

Casi todas las empresas evalúan a su proveedor de pagos basándose en una sola cifra: la comisión. Son muchos menos los que hacen una segunda pregunta que importa tanto como la primera: ¿cuándo llega realmente el dinero? En las redes de tarjetas, normalmente es T+2: dos días hábiles después de la venta. En las redes cripto es T+0: cuestión de minutos. Esa diferencia no es un tecnicismo. Es una palanca de flujo de caja que pasa desapercibida.

01 — La autorización no es la liquidación

La confusión comienza con el lenguaje. Cuando en el proceso de pago aparece "pago realizado con éxito", la mayoría asume que el dinero ya es suyo. No es así, al menos no todavía. Ocurren dos cosas distintas en momentos diferentes.

- La autorización es la decisión de sí o no sobre si el pago es válido. Ocurre en segundos, al finalizar la compra.

- La liquidación es el momento en que los fondos llegan realmente a tu cuenta, donde puedes disponer de ellos. En las redes de tarjetas, esto suele tardar dos días hábiles.

Y la expresión "días hábiles" es clave en esa frase. Una venta realizada el viernes por la noche no se liquida durante el fin de semana; contando la cola de procesamiento y el calendario bancario, el dinero puede llegar el martes o miércoles siguiente. Los ingresos existen, pero están en tránsito y no puedes disponer de ellos.

¿Por qué tarda dos días? La liquidación con tarjeta pasa por una cadena de intermediarios (el banco adquirente, las redes de tarjetas, el banco emisor), cada uno procesando y conciliando según su propio horario, dentro del horario bancario y con márgenes de riesgo integrados para permitir disputas. Nada de esto fue diseñado para la velocidad; se diseñó en torno a un sistema financiero anterior a internet, y el retraso de dos días es el residuo de ese diseño. No es un ajuste que tu proveedor pueda simplemente desactivar.

02 — Lo que T+2 te quita silenciosamente

Un retraso de dos días parece inofensivo en una sola venta. Pero en el conjunto de un negocio no lo es, porque nunca se detiene. Siempre hay un flujo constante de ventas atrapadas en el proceso de liquidación, y ese flujo representa dinero que has ganado pero que no puedes utilizar.

Tres factores se acumulan dentro de ese proceso:

- Capital flotante. Mientras tu dinero está en tránsito, genera intereses, generalmente para alguien en la cadena que no eres tú.

- Reservas rotativas. Los procesadores de tarjetas a menudo retienen un porcentaje de tus ingresos durante meses como medida de protección contra devoluciones de cargos, congelando capital mucho más allá de los dos días.

- Escalabilidad del volumen. Cuanto más vendes, mayor es el bloque permanente de capital atrapado en la liquidación. El crecimiento hace que el problema sea mayor, no menor.

03 — Qué cambia la liquidación T+0

La liquidación con criptomonedas funciona con otro ritmo. Una vez que un pago se confirma en la cadena, se liquida en cuestión de minutos, a cualquier hora y sin depender del calendario bancario. Una venta realizada un sábado a las 11 p. m. está disponible para su uso ese mismo sábado a las 11 p. m.

No hay capital flotante de dos días, ni pausas de fin de semana, ni esperas a que abra el banco el lunes. En una configuración sin custodia, los fondos llegan directamente a una billetera que tú controlas, listos para usarse en cuanto aparecen. El proceso que retenía una parte constante de tus ingresos simplemente desaparece.

Vale la pena ser precisos con el término "liquidado". Un pago en criptomonedas es definitivo una vez que cuenta con las confirmaciones que requiere tu proveedor: normalmente minutos, no días. A partir de ese momento, los fondos actúan como dinero en efectivo: sin estados pendientes, sin periodos de compensación y sin bancos que puedan revertirlos. Por fin, la liquidación significa lo que cualquier dueño de negocio siempre supuso que significaba.

04 — Cuál es el valor real de una liquidación más rápida

El valor se aprecia mejor con un modelo sencillo. Supongamos que procesas 100.000 $ al día. Con un sistema T+2, aproximadamente dos días de ventas —cerca de 200.000 $ siempre está en algún punto del proceso de liquidación: es dinero ganado, pero no disponible. Si pasas a T+0, esos 200 000 $ se convierten en capital de trabajo que realmente puedes utilizar.

Tus ingresos no han cambiado. No has vendido más. Simplemente has obtenido acceso a dinero que ya habías ganado dos días antes, todos los días. Lo que esto permite es concreto:

- Reinvierta en inventario o publicidad más rápido, para que el efectivo circule más veces al mes.

- Cubra la nómina y los pagos a proveedores con sus ingresos en lugar de recurrir a una línea de crédito.

- Reduzca la dependencia de una financiación cuya única función era cubrir el desfase de la liquidación.

Existe un segundo coste oculto bajo el primero: mientras tu dinero espera, no está inactivo. El capital flotante genera intereses y, en el sistema tradicional, esos intereses van a parar a los bancos y procesadores que retienen los fondos, no a ti. Muchas empresas cubren este desfase solicitando un préstamo de capital de trabajo o una línea de crédito renovable, pagando intereses por pedir prestado un dinero que ya han ganado y que simplemente están esperando recibir. Elimina el retraso en la liquidación y eliminarás la razón por la que ese préstamo existía en primer lugar.

Los mismos ingresos, antes. Una liquidación más rápida no aumenta los ingresos brutos. Devuelve el capital que tus ventas ya generaron, días antes, todos los días. Para una empresa que depende del flujo de caja, el tiempo no es un detalle; es la clave de todo.

Por qué el efecto es estructural y no puntual

El capital liberado no es una ganancia inesperada de una sola vez; es un cambio permanente en tu balance. Con T+2, siempre hay aproximadamente dos días de ingresos en tránsito, por lo que la cantidad retenida escala con tu ritmo de ventas y nunca desaparece. Cambia a T+0 y ese bloque se libera una vez y permanece así. A medida que creces, la brecha crece a tu favor, lo opuesto al modelo de tarjetas, donde escalar simplemente atrapa más capital en el proceso.

Calcula el impacto para tu negocio

La regla general es sencilla: volumen de pago diario promedio × días de liquidación eliminados = capital liberado. Una empresa que liquida 40 000 $ al día libera unos 80 000 $ al pasar de T+2 a T+0; una que liquida 500 000 $ al día libera aproximadamente un millón. Si añades cualquier reserva rotativa que retenga el procesador de tarjetas, la cifra aumenta aún más. No cuesta nada hacer tus propios cálculos: toma tu volumen diario de tarjetas, multiplícalo por dos y ese es el capital que actualmente está en tránsito y que una liquidación más rápida te devolvería.

05 — Donde la velocidad de liquidación es más importante

Dos días de espera son insignificantes para algunas empresas y decisivos para otras. El impacto es mayor cuando el efectivo necesita moverse con rapidez y frecuencia:

- Operaciones de alto volumen y márgenes reducidos — comercio minorista y mercados, donde unos pocos días de capital inmovilizado representan una cifra absoluta considerable.

- Alta rotación de inventario — empresas que necesitan los ingresos de ayer para reponer existencias hoy.

- Transacciones transfronterizas — la liquidación de tarjetas entre países es aún más lenta y costosa, mientras que las criptomonedas se liquidan a la misma velocidad en todas partes.

- Ingresos concentrados en fines de semana — sectores como el iGaming y el entretenimiento venden más precisamente cuando la liquidación de tarjetas se detiene; las criptomonedas no entienden de fines de semana.

Lo que estos casos tienen en común es un ciclo de efectivo corto: el dinero sale y necesita volver rápidamente para mantener el negocio en marcha. Cuanto más corto es ese ciclo, más duele un retraso de dos días, porque es un impuesto fijo sobre cada rotación. Una empresa que rota su capital dos veces al mes apenas nota dos días; una que lo rota cada pocos días siente el lastre constantemente.

06 — Más allá de la velocidad: previsibilidad y finalidad

La velocidad es solo la mitad de la ventaja. La liquidación T+0 también es más predecible — no hay que adivinar si se liquidará antes del festivo, porque no hay festivos que afecten a la liquidación. La planificación financiera se simplifica cuando el tiempo de llegada se mide en minutos en lugar de días hábiles.

También es definitiva. La liquidación en la cadena de bloques no se puede revertir, lo que elimina el riesgo de devoluciones de cargo y recuperaciones que obliga a los procesadores de tarjetas a mantener reservas rotativas. Y al liquidar en stablecoins como USDC o USDT significa que la velocidad no conlleva volatilidad: recibes un valor vinculado al dólar que se mantiene estable entre la venta y el momento en que lo utilizas.

En conjunto, la velocidad, la previsibilidad y la finalidad cambian la naturaleza misma del dinero que recibes. Los ingresos a T+2 son una reclamación : una promesa de que los fondos llegarán si nada sale mal en los próximos dos días. Los ingresos en stablecoins a T+0 son simplemente efectivo: ha llegado, es estable y no se puede revertir. Un equipo financiero puede planificar con el segundo tipo de una forma que nunca podrá hacer del todo con el primero.

"Las comisiones aparecen en la factura, por lo que reciben toda la atención. La velocidad de liquidación es invisible, y es la que decide cuánto de tu propio dinero puedes tocar realmente".

07 — Cuándo T+2 es suficiente

La velocidad de liquidación es una palanca, no un milagro, y conviene ser honestos sobre cuándo no marca la diferencia. Si tus volúmenes son pequeños, dos días de espera son un error de redondeo y una liquidación más rápida no cambiará tu negocio. Si al final necesitas que los fondos estén en una cuenta bancaria como dinero fiduciario, sigue existiendo el paso de salida (off-ramp), aunque mantener el valor en stablecoins reduce la urgencia de convertirlo inmediatamente.

En la práctica, la mayoría de las empresas no eligen una vía y abandonan la otra. Utilizan ambas y tratan las criptomonedas como el carril más rápido, barato y definitivo para los clientes que las usan, aprovechando el beneficio del flujo de caja donde está disponible sin renunciar a nada en otros aspectos.

También ayuda separar dos decisiones que a menudo se agrupan: liquidar rápido y mantener criptomonedas. No son la misma elección. Una empresa puede aceptar criptomonedas, liquidar en minutos y aun así convertir a dinero fiduciario según el calendario que prefiera. Lo que cambia es que el momento de esa conversión pasa a estar bajo tu control, en lugar de estar dictado por el calendario de una red de tarjetas y un reloj de dos días que tú nunca configuraste.

08 — Dónde encaja CPAY

Una ventaja en la velocidad de liquidación solo cuenta si el dinero está realmente disponible cuando llega. CPAY liquida los pagos en criptomonedas en minutos, en una billetera no custodiada que controla la empresa, con soporte para stablecoins y funciones integradas de pagos y envíos múltiples. El capital liberado por T+0 no queda bloqueado tras un custodio o una retención: es tuyo, disponible para gastar en el momento en que se liquida, a través de una API abierta y con transparencia en la cadena.

09 — Preguntas frecuentes

¿Qué significa la liquidación T+2?

T+2 significa que los fondos se liquidan dos días hábiles después de la transacción. Un pago autorizado el viernes puede no aparecer en su cuenta hasta el martes o miércoles siguiente, una vez que se cuentan los fines de semana.

¿La liquidación de criptomonedas es realmente instantánea?

Se liquida en minutos, las 24 horas del día, los 7 días de la semana, una vez que el pago se confirma en la cadena de bloques, sin depender del calendario bancario. Eso es lo que significa T+0 en la práctica: disponibilidad el mismo día, generalmente en el mismo minuto.

¿Cuánto capital de trabajo puede liberar una liquidación más rápida?

Aproximadamente su volumen de pago diario promedio multiplicado por los días de liquidación que elimina. Pasar de T+2 a T+0 libera cerca de dos días de ventas que antes siempre estaban en tránsito.

¿Una liquidación más rápida significa más riesgo?

No. La liquidación en la cadena de bloques es definitiva, lo que elimina el riesgo de devoluciones de cargo y recuperaciones. Los inconvenientes son el paso de salida a moneda fiduciaria y la volatilidad de los precios, ambos resueltos al liquidar en monedas estables.

¿Los fines de semana y días festivos afectan la liquidación de criptomonedas?

No. Las cadenas de bloques no cierran. Las criptomonedas se liquidan a la misma velocidad un domingo o un día festivo que un martes, lo cual es una gran parte de por qué la ventaja temporal se acumula.

Conclusión

Las comisiones acaparan toda la atención porque aparecen en la factura. La velocidad de liquidación no, pero es la que decide cuánto de sus propios ingresos puede utilizar realmente y cuándo. Pasar de T+2 a T+0 no aumenta las ventas; le devuelve el capital que esas ventas ya generaron, días antes, en cada transacción. Para una empresa que depende del flujo de caja, eso no es una funcionalidad. Es una palanca.

Tipo escriba aquí el pie de foto (opcional)